The Hidden Battle: Navigating Long-Term Disability Insurance Claims with Confidence

Long-term disability insurance claims can be a lifeline when illness or injury prevents you from working. While many people purchase disability coverage for peace of mind, the reality of filing and managing a claim can be far more complex than expected. Understanding how the process works and how to avoid common pitfalls can make a significant difference in securing the benefits you deserve.

What Is Long-Term Disability Insurance?

Long-term disability (LTD) insurance claim is designed to replace a portion of your income if you become unable to work due to a serious medical condition. Unlike short-term disability insurance, which typically covers a few months, LTD benefits can last for several years or even until retirement, depending on your policy.

These policies are commonly offered through employers, but individuals can also purchase private plans. Coverage usually begins after a waiting period—often 90 to 180 days—following the onset of a disability.

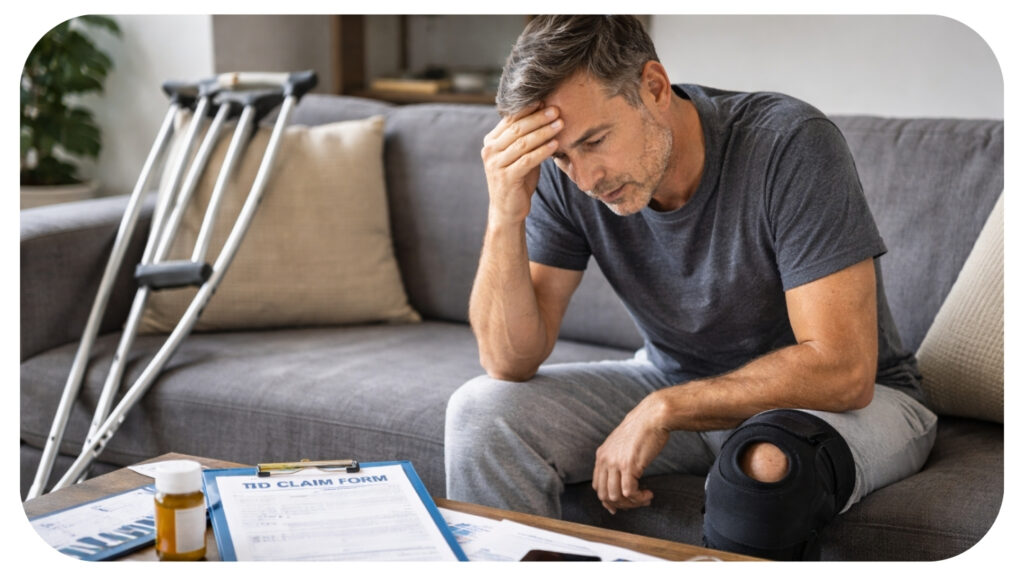

When Should You File a Claim?

Timing is critical when it comes to long-term disability insurance claims. You should file as soon as you realize your condition may prevent you from returning to work for an extended period. Delays can lead to complications, including denied benefits or gaps in income.

Before filing, review your policy carefully to understand eligibility requirements, waiting periods, and documentation needed. Many claims are denied simply because applicants fail to meet technical requirements or miss deadlines. You can also check this Victim sexual assault lawsuit in ontario

The Claims Process Explained

Filing a long-term disability insurance claim typically involves several steps:

1. Initial Application

The process begins with submitting a claim form to your insurance provider. This includes personal information, employment details, and medical documentation. Your employer and healthcare provider will also need to complete portions of the application.

2. Medical Evidence

Strong medical evidence is the backbone of any successful claim. Insurers require detailed records, including diagnoses, treatment plans, test results, and physician statements. Consistent and ongoing medical care is essential.

3. Review Period

After submission, the insurance company reviews your claim. This may involve consultations with medical professionals, vocational experts, or internal reviewers. The insurer evaluates whether your condition meets the policy’s definition of disability.

4. Approval or Denial

If approved, you will begin receiving monthly benefits based on your policy terms. If denied, the insurer must provide a reason, and you have the right to appeal.

Common Reasons Claims Are Denied

Understanding why long-term disability insurance claims are denied can help you avoid mistakes:

- Insufficient medical evidence: Lack of detailed or consistent documentation

- Failure to follow treatment plans: Non-compliance can weaken your case

- Missed deadlines: Late submissions can result in automatic denial

- Policy exclusions: Certain conditions may not be covered

- Disputes over disability definition: Insurers may argue you can still perform some type of work

Being proactive and thorough can significantly reduce the risk of denial.

The Importance of Medical Documentation

Your medical records play a central role in determining the outcome of your claim. It’s not enough to have a diagnosis—you must demonstrate how your condition limits your ability to work.

Regular visits to your healthcare provider, detailed symptom tracking, and clear communication about your limitations are essential. Ask your doctor to provide comprehensive reports that align with your policy’s definition of disability.

Employer-Sponsored vs. Private Policies

There are key differences between employer-sponsored and private LTD policies:

- Employer-sponsored plans are often governed by specific regulations and may have stricter deadlines and appeal processes.

- Private policies tend to offer more flexibility but may come with higher premiums and varying terms.

Understanding your policy type can help you navigate the claims process more effectively.

Tips to Strengthen Your Claim

To improve your chances of approval, consider the following strategies:

- Keep detailed records: Maintain copies of all medical reports, correspondence, and claim documents

- Communicate clearly: Ensure all forms are completed accurately and consistently

- Follow medical advice: Adhere to prescribed treatments and therapies

- Document your limitations: Keep a daily journal of how your condition affects your ability to work

- Seek professional guidance: Legal or insurance experts can help you avoid costly mistakes

What to Do If Your Claim Is Denied

A denial is not the end of the road. Many long-term disability insurance claims are approved on appeal. Here’s what you can do:

1. Review the Denial Letter

Understand the specific reasons for the denial. This will guide your appeal strategy.

2. Gather Additional Evidence

Strengthen your case with more detailed medical records, expert opinions, or vocational assessments.

3. File an Appeal

Follow the insurer’s appeal process carefully and meet all deadlines. This step is crucial for preserving your rights.

4. Consider Legal Assistance

An experienced professional can help you build a stronger case and navigate complex regulations.

The Role of Insurance Companies

Insurance companies are businesses, and their goal is to manage risk and minimize payouts. This doesn’t mean they act unfairly, but it does mean you should approach the claims process with diligence and preparation.

Understanding how insurers evaluate claims can give you an advantage. They look for consistency, credibility, and clear evidence that your condition prevents you from working.

Emotional and Financial Impact

Dealing with a long-term disability is challenging enough without the added stress of navigating an insurance claim. Financial uncertainty, medical expenses, and the loss of routine can take a toll on your mental health.

Having a clear plan and support system can help you manage these challenges more effectively. Don’t hesitate to seek help from professionals, family, or support groups.

Final Thoughts

Long-term disability insurance claims are more than just paperwork—they represent a crucial safety net during some of life’s most difficult moments. By understanding the process, staying organized, and advocating for yourself, you can improve your chances of a successful outcome.

Preparation is key. The more informed and proactive you are, the better equipped you’ll be to handle the complexities of your claim and secure the benefits you need to move forward with confidence.

Most Inside Editorial Team

MostInside is an independent publication focused on growth across lifestyle, business, finance, sports, and digital authority, prioritizing long term value and enduring credibility.